The global semiconductor packaging market is projected to reach $618.9 billion this year, driven by strong growth in AI servers and electric vehicles, according to KPCA.

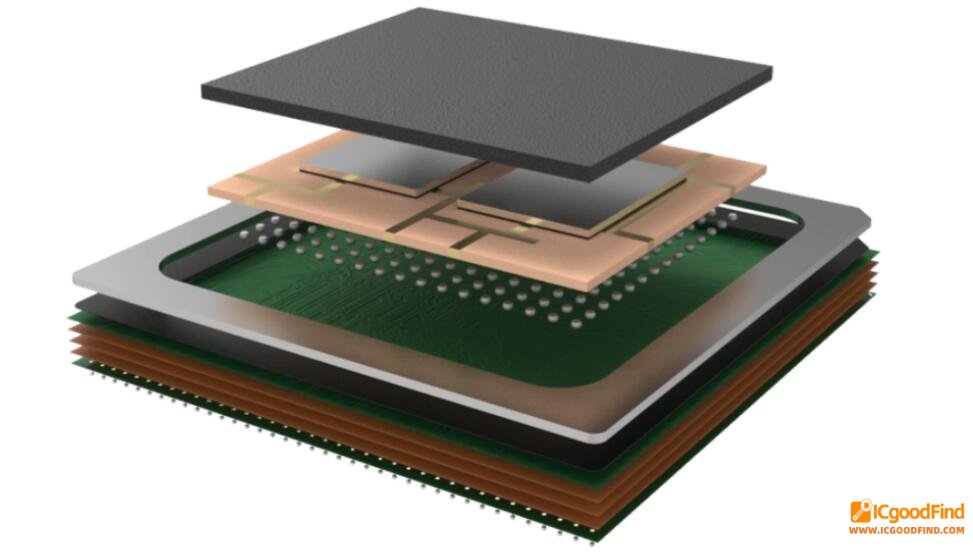

AI servers are a key growth engine, with CAGR exceeding 20%. Demand for HBM, 2.5D stacking, 3D stacking, and heterogeneous packaging continues to surge. The industry focus is shifting from front-end scaling to advanced back-end packaging.

FC-BGA and 2.5D packaging are now widely used in ADAS and autonomous driving controllers, meeting strict automotive reliability and thermal requirements.

The OSAT market remains highly concentrated, with top ten players holding 80% share. Taiwan and China together account for 70%. Korea is aggressively expanding in HBM and CoWoS, while 2.5D/3D packaging is expected to grow over 30% annually.

Challenges include volatile raw material prices (copper, resin) and heavy reliance on imported CCL and prepreg materials.

KPCA notes that the industry is moving toward deeper integration of advanced packaging, high-end substrates, and core materials, with glass substrates and high-layer IC substrates set to accelerate future upgrades.

ICgoodFind: AI and automotive electronics drive packaging market past $600B, but material supply chains remain a critical test.